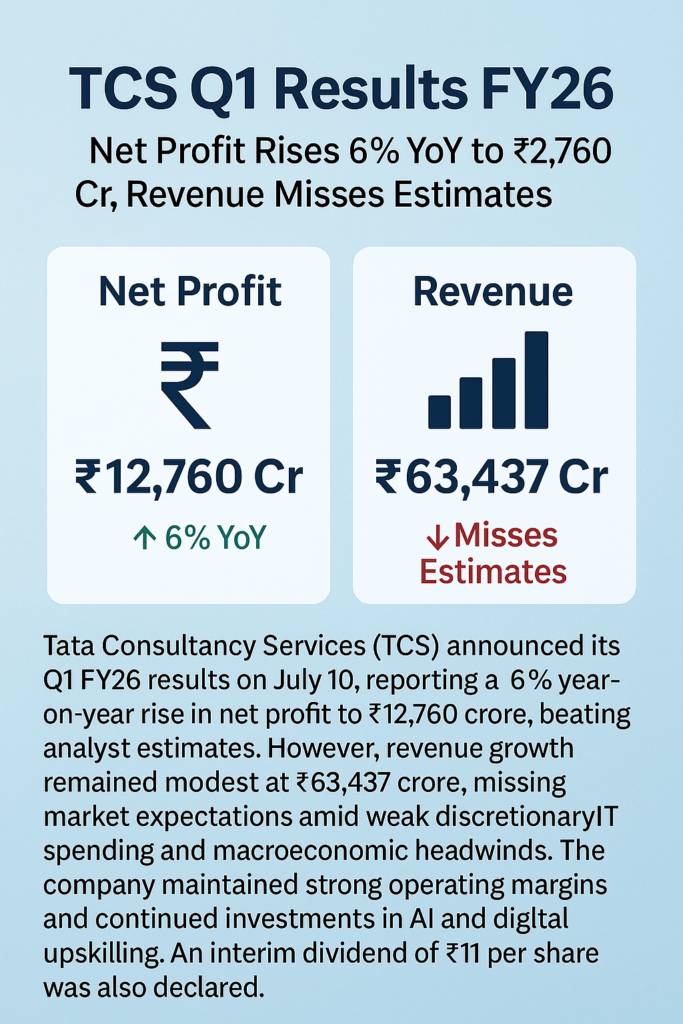

Tata Consultancy Services (TCS) announced its Q1 FY26 results on July 10, reporting a 6% year-on-year rise in net profit to ₹12,760 crore, beating analyst estimates. However, revenue growth remained modest at ₹63,437 crore, missing market expectations amid weak

discretionary IT spending and macroeconomic headwinds. The company maintained strong operating margins and continued investments in AI and digital upskilling. An interim dividend of ₹11 per share was also declared

https://digitalinternational.in/

Margins & Operational Metrics

EBIT Margin: 24.5%, up 30 bps QoQ from 24.2%

Net Margin: Approximately 20.1% .

Deal Wins (TCV): $9.4 bn, down from $12.2 bn in Q4

Headcount Growth: Added 6,071, total employees 613,069; attrition rate up to 13.8%

Cash from Operations: ₹12,804 cr .

Strategic Actions & Commentary

Dividend Declared: Interim dividend of ₹11/share; record date July 16, payout scheduled August 4, 2025

AI & Skill Investment: 15 million training hours; 114,000 employees with higher-order AI skills

Leadership Take: CEO K Krithivasan noted macroeconomic and geopolitical uncertainties dented demand, though new services performed well. CFO Samir Seksaria highlighted steady margins and strategic investment for sustainable growth

https://digitalinternational.in/

Financial Performance

Net Profit (PAT): ₹12,760 cr, up 6% YoY (from ₹12,040 cr) — ahead of analyst estimates (~₹12,253 cr

Revenue from Operations: ₹63,437 cr, a modest 1.3% rise YoY (₹64,600 cr). In constant currency terms, revenue declined ~3.1% YoY

DIGI MERCH STORE PRINT ON DEMAND

Analyst & Market Reaction

Revenue shortfall attributed to lower discretionary spending and the tapering of a major BSNL deal (~$1.83 bn)

Most analysts expected flat-to-slight revenue growth but margins held firm due to wage deferments and currency benefits.

TCS shares responded mildly, with the stock closing slightly lower after results

Comment: