SAVE Student Loan Program Update: New Timeline Offers Relief to Borrowers

Millions of borrowers enrolled in the SAVE student loan repayment plan have received a temporary reprieve as the U.S. Department of Education extends the transition deadline into late 2026.

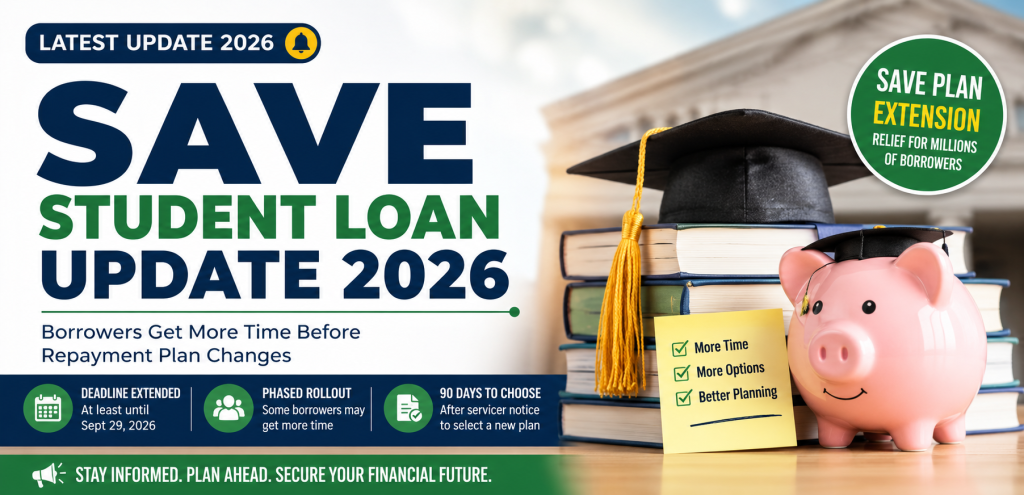

Millions of Americans enrolled in the Saving on a Valuable Education (SAVE) student loan repayment plan have received temporary relief after the U.S. Department of Education extended the timeline for transitioning borrowers to new repayment options. The decision provides additional time for federal student loan borrowers as legal challenges surrounding the SAVE program continue and officials work toward implementing a long-term repayment strategy.

For millions of student loan borrowers across the United States, the latest announcement represents welcome news after months of uncertainty. Borrowers who were concerned about immediate changes to their monthly payments now have additional time to prepare, understand their options, and make informed financial decisions.

What Is the SAVE Student Loan Repayment Plan?

The Saving on a Valuable Education (SAVE) Plan is a federal income-driven repayment (IDR) program created to help borrowers make affordable monthly payments based on their income and family size.

Unlike traditional repayment plans that calculate fixed monthly payments, the SAVE Plan was designed to reduce financial pressure by ensuring borrowers pay only what they can reasonably afford. In many cases, monthly payments were significantly lower than under previous income-driven repayment plans.

The plan also included protections against unpaid interest growth for eligible borrowers, preventing loan balances from increasing when monthly payments were too low to cover accrued interest. These features made the SAVE Plan one of the most widely used federal repayment programs shortly after its introduction.

Why Has the SAVE Plan Been Delayed?

Although the SAVE Plan helped millions of borrowers, it quickly became the subject of legal challenges. Several states filed lawsuits questioning whether the federal government had the legal authority to implement portions of the repayment program. Court rulings and ongoing litigation have created uncertainty about the future of the plan.

Because the legal process remains unresolved, the Department of Education decided to extend the transition period rather than require borrowers to immediately move into different repayment plans. Officials say the extension will allow more time to complete administrative work while courts continue reviewing the legal issues surrounding the program.

New Transition Timeline

According to the latest federal guidance, borrowers currently enrolled in the SAVE Plan will not be required to leave the program until at least late September 2026. Rather than moving every borrower at once, the Department of Education plans a phased transition. This means that some borrowers may remain in the SAVE Plan even longer depending on their loan servicer and individual circumstances.

Borrowers should continue monitoring official communications from their loan servicer because transition dates may differ from one account to another.

What Borrowers Should Expect

For now, most SAVE borrowers do not need to take immediate action. When the transition officially begins, loan servicers are expected to contact borrowers with instructions explaining:

- Available repayment plans

- Monthly payment estimates

- Enrollment deadlines

- How to switch repayment options

- Required documentation

Borrowers will generally receive approximately 90 days to choose a new repayment plan after being notified. If no repayment option is selected before the deadline, loan servicers may automatically place borrowers into another eligible repayment plan based on federal guidelines.

Available Repayment Options

Once borrowers leave the SAVE Plan, they may be eligible for several federal repayment programs.

- Income-Based Repayment (IBR)

- Income-Contingent Repayment (ICR)

- Pay As You Earn (PAYE), for eligible borrowers

- Standard 10-Year Repayment Plan

- Graduated Repayment Plan

- Extended Repayment Plan

Each repayment option has different eligibility requirements, monthly payment calculations, and forgiveness rules. Borrowers should compare repayment plans carefully before making a decision.

Impact on Public Service Loan Forgiveness

The SAVE Plan has been especially important for borrowers working toward Public Service Loan Forgiveness (PSLF). Teachers, nurses, military personnel, firefighters, police officers, and nonprofit employees often rely on income-driven repayment plans while earning qualifying payments toward eventual loan forgiveness.

Although the SAVE transition has created uncertainty, borrowers pursuing PSLF should continue maintaining employment certification records and monitoring guidance from the Department of Education. Experts recommend avoiding unnecessary repayment plan changes until official instructions are received.

Financial Planning During the Extension

The additional transition period gives borrowers valuable time to strengthen their financial position.

- Review current household income

- Update contact information with loan servicers

- Check federal student loan balances

- Estimate future monthly payments

- Build emergency savings

- Understand available repayment programs

Preparing early may reduce financial stress once the transition officially begins.

Why This Matters for Millions of Americans

Student loan debt continues to affect millions of households throughout the United States. Monthly loan payments influence housing decisions, retirement savings, family budgets, and career choices.

Any change to federal repayment policies therefore has a significant impact on borrowers’ financial planning. The SAVE extension provides temporary stability while policymakers, courts, and federal agencies determine the long-term future of income-driven repayment programs.

Ongoing Legal Developments

The legal disputes involving the SAVE Plan remain active.

- Income-driven repayment policies

- Monthly payment calculations

- Loan forgiveness eligibility

- Administrative procedures

- Future repayment plan availability

Because litigation is ongoing, borrowers should avoid relying on unofficial information shared through social media or unverified online sources. Instead, they should follow updates from the U.S. Department of Education and their loan servicer.

Preparing for the Future

Although the extension delays immediate changes, borrowers should not assume the SAVE Plan will remain unchanged indefinitely. The Department of Education has indicated that additional guidance will be released as legal proceedings continue and administrative plans develop.

Borrowers should remain proactive by reviewing repayment options, keeping personal information current, and responding promptly to official notices. Understanding available repayment choices before deadlines arrive can make the transition smoother and help borrowers avoid unnecessary payment issues.